Why I Decided to Stop Ignoring My Credit Score

Are You Just Paying Interest… Not Your Debt?

Most people don’t realize this… but minimum payments are designed to keep you stuck for years. You could be paying hundreds every month and barely touching what you actually owe.

👉 If you have $5,000+ in debt, there may be options to reduce what you owe and get out faster.

Takes less than 2 minutes. No pressure, just see your options.

Why I Decided to Stop Ignoring My Credit Score

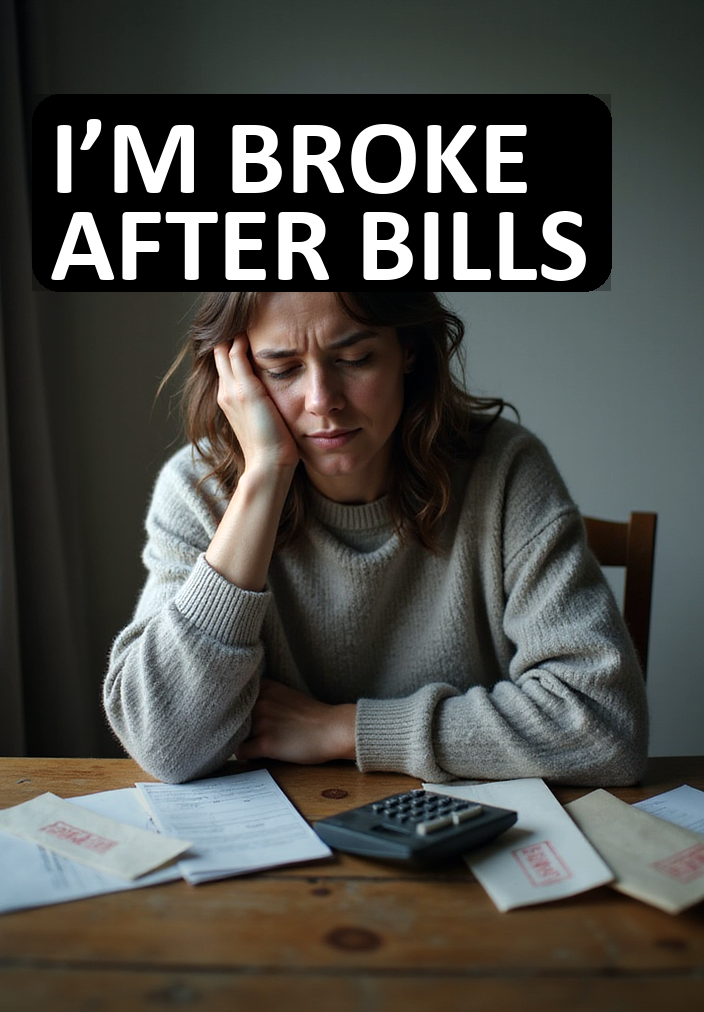

For years, I found myself living in a cycle of avoidance when it came to my credit score. Ignoring it felt easier than facing the financial reality that seemed to loom over me. I wasn’t alone; many of us find ourselves caught in a web of debt, credit card bills, and personal loans, feeling overwhelmed and powerless. But ignoring my credit score only allowed the stress to build quietly, impacting both my finances and my mental well-being. It took a moment of reflection for me to realize how much of my life was being affected by this lingering debt pressure. Here’s how I made the decision to confront my credit score instead of running away from it.

The Quiet Build-Up of Debt

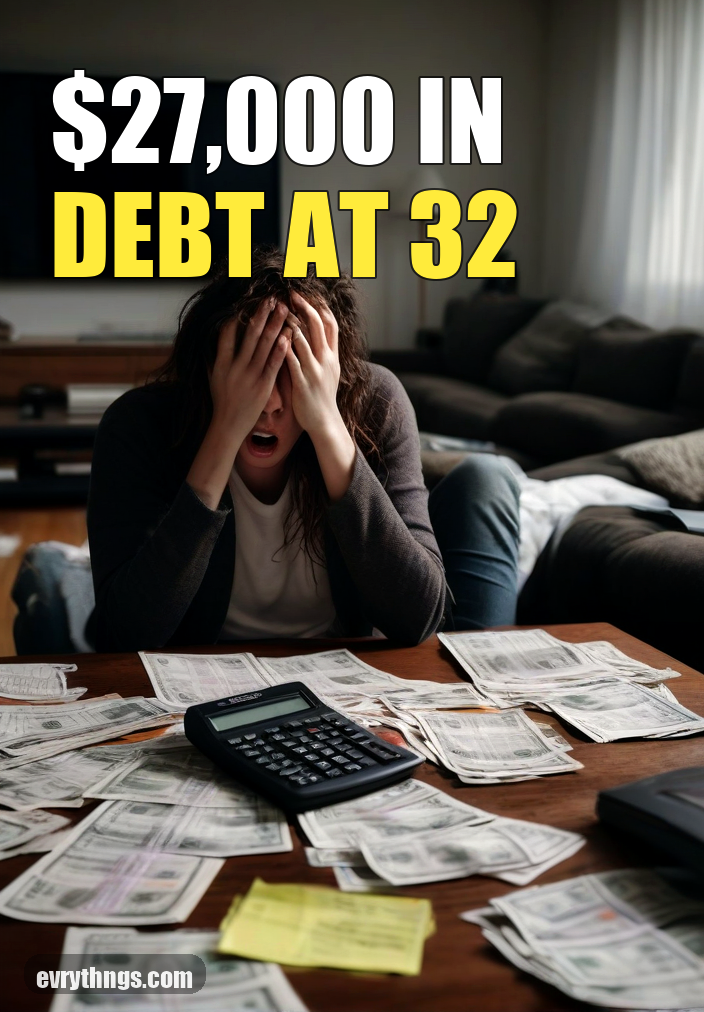

Debt doesn’t shout; it whispers. It creeps into our lives slowly, often starting with a small purchase or a single missed payment. Before I knew it, my once manageable credit card balance had ballooned, and I was drowning in interest rates. The minimum payments felt more like a lifeline than a solution. Every month, I’d send off my payment, only to watch my debt remain stagnant or even grow. This cycle of minimum payments led me to avoid looking at my credit score, as the numbers only served to remind me of my financial shortcomings.

The Interest Trap

Debt Doesn’t Just Sit There… It Grows

Interest stacks every month. Late fees pile up. And before you know it, what started small turns into something that feels impossible to get out of.

The difference between people who stay stuck and people who get out? They actually check what options are available instead of guessing.

👉 You could qualify to reduce your total debt and lower your monthly payments.

No commitment. Just see what’s possible in minutes.

One of the most insidious aspects of credit card debt is how interest compounds. It’s not just the amount you owe; it’s the ever-growing mountain of interest that steadily attaches itself to your balance. I remember the sinking feeling when I realized that with each passing month, I was paying more in interest than I was chipping away at the principal. The emotional strain that came with seeing my balance barely budge was demoralizing. I felt powerless, and that powerlessness only made the cycle worse.

Facing the Emotional Realities

Ignoring my credit score wasn’t merely a financial decision; it was a deeply emotional one. Shame played a pivotal role in my avoidance. I’d scroll through financial articles, each one more intimidating than the last, and I’d feel a sense of defeat wash over me. I convinced myself that others had their finances together, while I was stuck in this miserable pit of debt. The stress bled into my relationships, too. I’d find myself avoiding discussions about money, fearing judgment from friends or family. This cycle of avoidance only deepened my sense of isolation.

Acknowledging the Pressure

Financial pressure is often intertwined with emotional pressure. The constant worry about bills and payments can lead to sleepless nights and strained relationships. I started to recognize that my avoidance was not just about my credit score; it was about my overall well-being. By confronting my credit score, I was also confronting the emotional weight I had been carrying. It became clear that ignoring the issue was affecting my peace of mind and my happiness.

Taking the First Steps

In the midst of this emotional turmoil, I knew I needed a strategy. Ignoring my credit score was not the answer; I had to take action. I began by simply checking my credit report. This step, while daunting, was a revelation. I was finally facing the numbers that had haunted me. I took the time to understand what impacted my score and what steps I could take to improve it. It was daunting to confront those figures, but it was also liberating. I no longer felt like a victim of my circumstances; I was taking ownership of my financial situation.

Seeking Help

For those of us grappling with serious debt, seeking help can be a vital step. I discovered various resources, including debt relief consultations, that can provide guidance and support. One option I found was CuraDebt, which offers consultations for those with significant unsecured debt. While it’s not a miracle fix, it can be a helpful resource for anyone feeling overwhelmed. The important part is recognizing that reaching out for help is a sign of strength, not weakness.

Finding Hope and Moving Forward

Recognizing my credit score felt like peeling back the layers of a problem I had long avoided. It was a daunting process, but it also opened the door to hope. Confronting my financial reality allowed me to take tangible steps towards improvement. I learned to set realistic goals for my finances, focusing on one manageable step at a time instead of succumbing to the pressure that had once paralyzed me.

If you’re feeling the weight of debt, I encourage you to take that first step. Whether it’s checking your credit score, acknowledging your financial situation, or seeking help from a service like CuraDebt, know that you are not alone. The journey to financial wellness may be challenging, but it’s within reach. You have the power to change your situation, starting today. Take a deep breath, acknowledge your feelings, and make a plan. You can do this.

You Can Keep Struggling…

Or Actually Do Something About It

Most people leave this page and go right back to stressing about bills, minimum payments, and growing balances.

Or… you can take 2 minutes right now and see if there’s a real way out.

✔ Free consultation

✔ See if you qualify for debt reduction

✔ No pressure — just real options

Takes less than 2 minutes to check. Nothing to lose.