The Hidden Costs of Living with Unpaid Debt

Are You Just Paying Interest… Not Your Debt?

Most people don’t realize this… but minimum payments are designed to keep you stuck for years. You could be paying hundreds every month and barely touching what you actually owe.

👉 If you have $5,000+ in debt, there may be options to reduce what you owe and get out faster.

Takes less than 2 minutes. No pressure, just see your options.

The Hidden Costs of Living with Unpaid Debt

Debt often creeps into our lives in a way that feels almost benign at first. Perhaps it starts with a small credit card balance, a personal loan to cover unexpected expenses, or a few missed payments that you think you can quickly catch up on. However, as time passes, the true costs of these financial choices begin to unfold, often leading to greater stress and emotional turmoil than we initially anticipated. Understanding the hidden costs of living with unpaid debt is essential for anyone navigating these turbulent waters.

How Debt Quietly Accumulates

One of the most insidious aspects of debt is its tendency to build up quietly. You might not notice the gradual increase in your credit card bill until it reaches a point where making the minimum payment feels overwhelming. Interest compounds, often at rates that seem barely noticeable until they add a significant amount to what you owe. What starts as a manageable monthly payment can soon morph into a larger financial burden, feeding the cycle of stress and anxiety.

The Trap of Minimum Payments

Debt Doesn’t Just Sit There… It Grows

Interest stacks every month. Late fees pile up. And before you know it, what started small turns into something that feels impossible to get out of.

The difference between people who stay stuck and people who get out? They actually check what options are available instead of guessing.

👉 You could qualify to reduce your total debt and lower your monthly payments.

No commitment. Just see what’s possible in minutes.

Many people fall into the trap of focusing solely on making minimum payments. While this can feel like a manageable approach, it’s important to understand the long-term implications. Minimum payments are designed to keep you in debt longer, as they cover only a fraction of your total balance, primarily the interest. What might feel like a small step toward managing your finances can actually prolong your struggle, leading to years—if not decades—of repayment. This delay in getting ahead financially can weigh heavily on your mental and emotional well-being, creating a persistent sense of insecurity and stress.

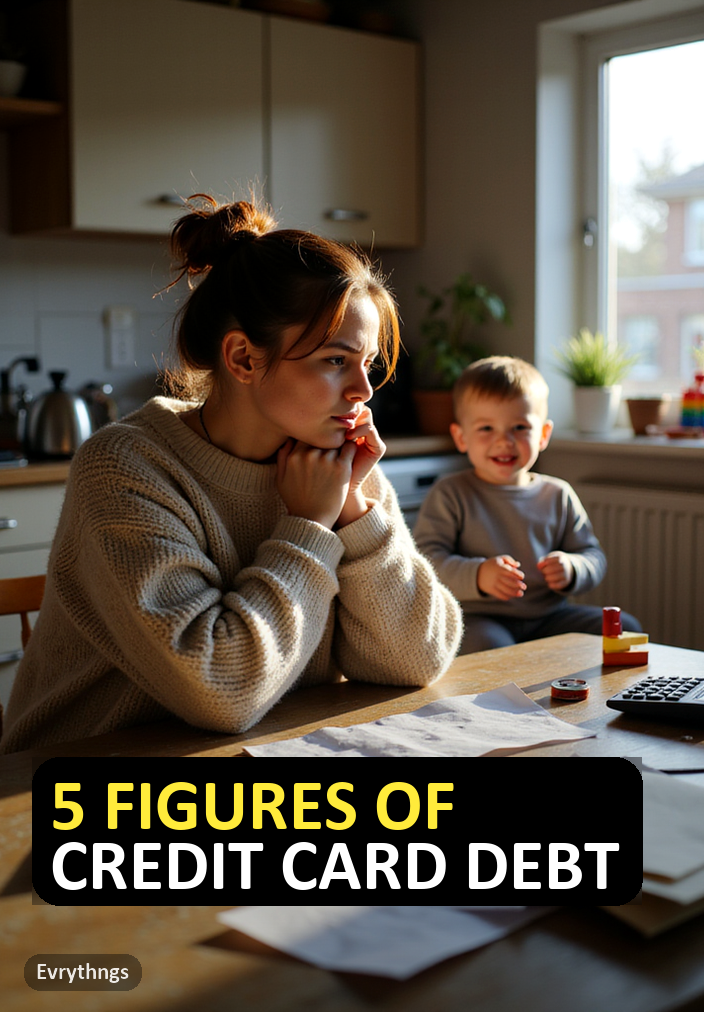

The Emotional Toll of Debt

Living with unpaid debt can evoke a wide range of emotions, from shame and guilt to anxiety and hopelessness. It’s not uncommon for individuals to avoid thinking about or discussing their financial situation. This avoidance, however, often leads to increased stress and feelings of isolation. The fear of judgment from friends or family can make it even harder to seek help, trapping you in a cycle of silence and struggle.

Shame and Avoidance

The emotional weight of debt can manifest as shame, making you feel as if you’ve lost control of your financial life. This feeling can lead to avoidance behaviors, such as neglecting bills, ignoring collection calls, or even hiding from friends and family. It’s crucial to acknowledge these feelings rather than push them aside. Recognizing the emotional impact of debt is a key step in addressing the situation and moving toward a healthier financial mindset.

Stress and Relationship Pressure

Debt doesn’t just impact your personal well-being; it can strain your relationships, too. Financial stress is a leading cause of tension in partnerships and family dynamics. Conversations about money can quickly turn into arguments, leading to feelings of resentment and frustration. It’s important to remember that you’re not alone in this; many people face similar struggles. Open communication with loved ones can help alleviate the burden of secrecy and shame and foster a supportive environment for addressing financial challenges together.

Practical Steps Toward Financial Relief

While the emotional and psychological effects of debt are very real, there are practical steps you can take to address your situation. The first step is often the hardest—acknowledging the reality of your debt. Once you’ve done that, consider creating a clear overview of your financial situation. Start by listing your debts, including interest rates and minimum payments. This clarity can help you see the whole picture and motivate you to take action.

Exploring Your Options

Once you have a grasp on your finances, it may be helpful to explore your options for debt relief. Whether you choose to negotiate directly with creditors, consider a debt management plan, or even seek professional assistance, knowing that there are paths to relief can instill a sense of hope. For those facing serious unsecured debt, a service like CuraDebt can provide personalized consultations and help you understand potential solutions tailored to your situation. Just remember, this isn’t a miracle fix, but rather a way to explore your options and make informed decisions.

A Call to Action

As you navigate this challenging terrain, I encourage you to take one concrete step today. Whether it’s reaching out to a trusted friend to share your burden, researching debt relief options, or setting up a consultation with a service like CuraDebt, taking action can help you regain a sense of control. The first step doesn’t have to be monumental; it just needs to be a step forward.

Finding Hope Amidst Debt

Living with unpaid debt can feel overwhelming, but it’s important to remember that you have the power to change your financial narrative. Acknowledge the reality of your situation, seek support, and take gradual steps toward financial health. Each small action counts and can lead to greater peace of mind. You’re not alone on this journey, and taking that first step can lead you towards a brighter, more hopeful financial future. Remember, you deserve to feel secure and empowered in your financial life.

You Can Keep Struggling…

Or Actually Do Something About It

Most people leave this page and go right back to stressing about bills, minimum payments, and growing balances.

Or… you can take 2 minutes right now and see if there’s a real way out.

✔ Free consultation

✔ See if you qualify for debt reduction

✔ No pressure — just real options

Takes less than 2 minutes to check. Nothing to lose.