The Real Cost of Paying Only the Minimum on My Credit Cards

Are You Just Paying Interest… Not Your Debt?

Most people don’t realize this… but minimum payments are designed to keep you stuck for years. You could be paying hundreds every month and barely touching what you actually owe.

👉 If you have $5,000+ in debt, there may be options to reduce what you owe and get out faster.

Takes less than 2 minutes. No pressure, just see your options.

Understanding the Impact of Minimum Payments on Credit Card Debt

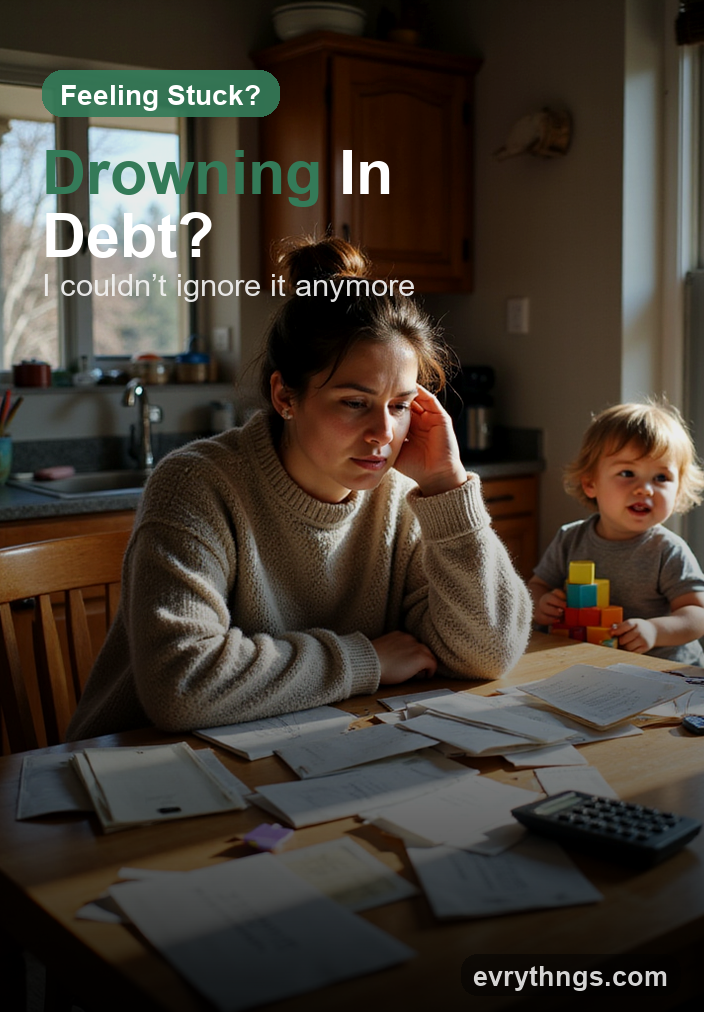

For many, credit cards can feel like a double-edged sword. On one hand, they offer a convenient method for making purchases; on the other, they can lead to a cycle of debt that feels impossible to escape. As you glance at your monthly statements, you might notice the option to pay only the minimum amount due. It seems tempting, right? After all, it allows you to get by, at least for now. But have you ever stopped to consider the real cost of that decision?

The Quiet Build-Up of Debt

One of the most insidious aspects of credit card debt is how quietly it builds over time. You might start with a small balance, but as interest accumulates—often at alarming rates—that small amount can grow into a substantial burden. Each month, when you opt to pay only the minimum, you’re essentially saying, “I’ll deal with this later.” But later can quickly turn into years. A $1,000 balance at a 20% interest rate, for example, can take more than five years to pay off if you only pay the minimum. You could end up paying more than $1,200 just to clear that initial debt.

The Role of Interest

Debt Doesn’t Just Sit There… It Grows

Interest stacks every month. Late fees pile up. And before you know it, what started small turns into something that feels impossible to get out of.

The difference between people who stay stuck and people who get out? They actually check what options are available instead of guessing.

👉 You could qualify to reduce your total debt and lower your monthly payments.

No commitment. Just see what’s possible in minutes.

Interest is the silent partner in your financial relationship with credit cards. While it can sometimes feel like a minor detail—just a percentage tacked on to your balance—it has a powerful impact. Each month, your lender applies interest to your remaining balance, and if you’re only making minimum payments, that interest keeps compounding. What’s more, many people don’t realize that their minimum payments often barely cover the interest accrued, meaning they are making little to no progress on paying down the principal. This realization can be both frustrating and overwhelming.

The Trap of Minimum Payments

Choosing to pay only the minimum may seem like an easy way to manage your financial responsibilities, but it can quickly lead to a vicious cycle of financial stress. With every payment, you might feel a sense of temporary relief, but that feeling is often short-lived. The truth is, the smaller payments allow the debt to linger, which can lead to a growing sense of anxiety about your finances.

Emotional Realities of Debt

Living with debt can feel isolating. It’s common to experience deep feelings of shame or embarrassment, and many people avoid discussing their financial situations even with their closest friends or family. This avoidance only amplifies feelings of stress and anxiety. You may find yourself lying awake at night, worrying about mounting bills, or feeling burdened by the weight of financial expectations in your relationships.

The pressure can be especially acute if you feel responsible for your family’s well-being or financial stability. You might find yourself stuck in a cycle of justifying purchases or convincing yourself that “just one more month” of minimum payments won’t hurt. But the reality is that every month you delay addressing the debt contributes to greater stress and emotional turmoil.

Finding a Path Forward

If you’re feeling overwhelmed by credit card debt, it’s essential to recognize that you’re not alone. Many people are grappling with similar feelings of stress and anxiety. The key is taking small, actionable steps toward financial relief. Ignoring the problem won’t make it go away; it will only add layers to the already complex emotional and financial burdens.

Exploring Debt Relief Options

In your journey to tackle your credit card debt, you might consider reaching out to a professional for help. Services like CuraDebt offer consultations to discuss your options based on your financial situation and can help map out a realistic path toward debt relief. Remember, this isn’t a miracle fix, but it’s one step you can take to regain control over your financial future.

Concluding Thoughts: Taking That First Step

It’s easy to feel trapped in a cycle of minimum payments, but it’s crucial to remember that there is hope. You don’t have to face this alone. The first step doesn’t need to be monumental; it can be as simple as reviewing your financial statements or reaching out for help. Acknowledge your feelings, face your financial situation with a sense of courage, and remember that taking action—no matter how small—can lead to a brighter financial future. You are capable of more than you might believe, and the journey begins by taking just one step forward.

You Can Keep Struggling…

Or Actually Do Something About It

Most people leave this page and go right back to stressing about bills, minimum payments, and growing balances.

Or… you can take 2 minutes right now and see if there’s a real way out.

✔ Free consultation

✔ See if you qualify for debt reduction

✔ No pressure — just real options

Takes less than 2 minutes to check. Nothing to lose.